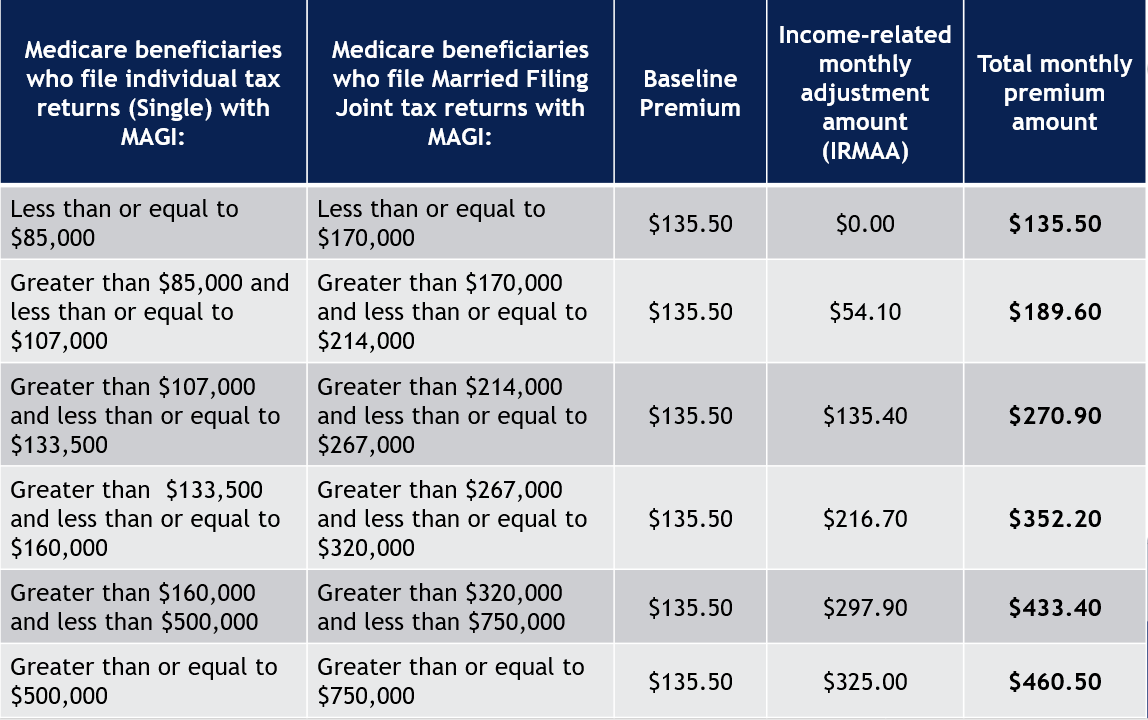

Did you know that a portion of your Medicare premium is determined by your income? It’s true! Medicare Part B, which largely covers doctor’s visits, ambulance services, durable medical equipment, chiropractic care, and outpatient therapy, is based on your Modified Adjusted Gross Income (MAGI). MAGI is a fancy IRS term for total income before any deductions. When your income is above certain levels, the IRS can enforce an Income-Related Monthly Adjustment Amount (IRMAA) on your Medicare Part B Premium. They do so by looking at your prior-prior year’s tax return (your 2019 Medicare premium is based on your 2017 MAGI) and if your income was “too high”, they send you a letter notifying you that your premium is going up – sometimes by as much as $325/month. You can also see from the chart below that a change from Married Filing Jointly to Single can result in a nasty premium increase due to being widowed (or divorced). If your MAGI is just $1 above an income limit, you will be charged the full IRMAA amount for an entire year! Below is a schedule of the important income limits.

If you find yourself close to the border of one of the income thresholds, there are a couple of things you could do to stay under the limit or potentially even get under the limit if you are already above.

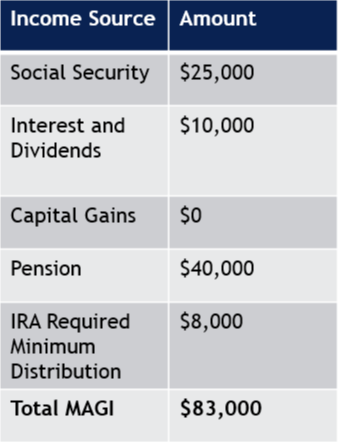

To illustrate, let’s use Frank as an example. Frank is single, 72 years old, and has the following MAGI:

Currently, Frank is over the limit by $2,000 which, if he does nothing, will cost him $649 each year going forward. What can he do?

Nothing, he better get used to it! No! Come on! He has smart advisors working for him - he has a couple of options.

- Let’s assume Frank gives $200/month to his church. Instead of him putting a cash envelope into the collection plate each week, he can have the money come out of his retirement account and be paid directly to the church. By doing so, he reduces his MAGI by $2,400 which puts him under the income limit. This saves him $649/year by just changing how he gives to his church! Assuming Frank is in the 22% tax bracket, he will also save an additional $528 in federal income taxes, for a total savings of $1,177! Two things make this strategy work. One is that Frank is over 70.5 which is the age at which the IRS requires annual distributions from IRA accounts. The second is that Frank takes the standard deduction on his tax return because it is larger than the sum of his itemized deductions (which include charitable donations). This means he doesn’t receive a tax deduction for any cash donations to his church via the collection plate. The Tax Foundation estimates that 88% of tax filers will use the standard deduction (like Frank) given the recent changes to the tax law.

- Now let’s assume Frank does not make any charitable donations but he does have a non-retirement investment account with stocks and bonds in it. This is the account above that is generating $10,000 per year in interest and dividends. Inside of his account he has positions that have gained value and some that lost value. If he has positions with losses, he could sell some of those and take up to a $3,000 loss each year. If he does that, that will also put him under the IRMAA limit. There are also ways for him to stay invested and take the loss without sacrificing his position in the investment.

These are just a few options Frank could use to help make his retirement income plan more efficient.

Finally, let’s assume Frank’s MAGI looks like this:

In this case, Frank’s MAGI is below $85,000 which puts him under the limit for the IRMAA increase. But he’s having issues with his roof and decides he needs to get it repaired. Frank isn’t an expert on retirement income planning, so he processes a $6,000 distribution out of his IRA to help pay for the cost. This distribution pushes him up to $89,000 of MAGI. Frank is going to be mad in 2021 when he gets a letter saying he now needs to pay an additional $649/year for Medicare! Had Frank took the $6,000 out of his non-retirement account, he may have been able to save the $649.

As you can see, it is very important to keep an eye on your income in retirement. If not, you could wind up paying more for benefits you’ve already paid for!

If you have questions about your specific situation, please feel free to give our office a call. If you’d like to schedule an appointment please click here.