A 401(k) has proven to be a great tool to accumulate wealth over time by providing an easy way for workers to save and the ability for employers to match contributions. The investment decision has been a fairly easy one – invest aggressively while you are young and become more conservative as you get older. Strong stock and bond markets have rewarded investors and allowed 401(k) assets to top $7 trillion since the inception of the 401(k) in 1978. However, what has worked in the past may not work in the future.

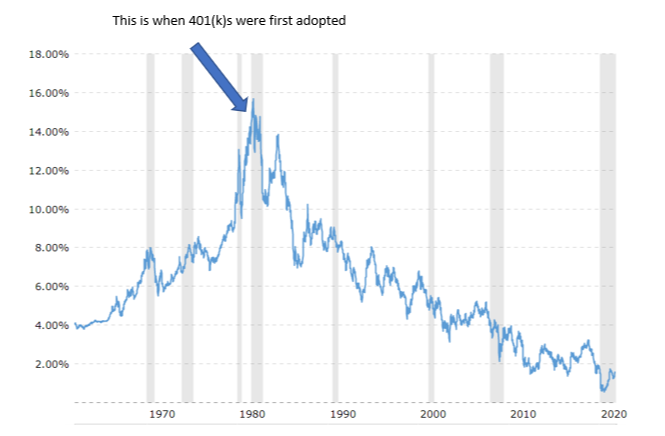

As older workers transition their aggressive investments to more conservative investments, they now face historically low interest rates. Interest rates have been falling since 1981 when the 10-year government bond rate peaked at 13.92%. The current 10-year government bond rate sits at about 1.5%.

10 Year US Government Bond Chart

Source: Macrotrends.net

While low interest rates are great for borrowers, they are terrible for conservative investors, especially in times like these where we are seeing the costs of goods and services (inflation) increase at over 5% per year. If inflation is 5% and you earn a 1.5% rate of return on your conservative investments, your money will only purchase 96.5% of the products it could the year before. This can get ugly fast.

Let’s assume you have $1,000,000 invested in your 401(k) and because you are getting close to retirement you decide to make your investments more conservative by investing primarily in bonds. After 10 years, assuming inflation runs at 5% per year, your million would need to grow to $1,551,328 to maintain the same level of wealth. At a 1.5% rate of return, your million “grows” to $1,143,389 but now can only buy 73% of the stuff it could before.

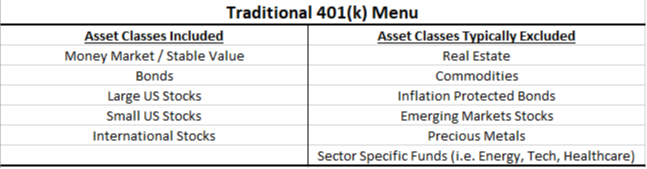

So, what can investors do to protect against inflation? Historically, stocks are a good way to protect against inflation as well as other asset classes like real estate, commodities, and inflation-protected bonds. As investment advisors, the problem we are seeing today is the availability of these asset classes in 401(k) investment menus is severely limited.

Most 401(k) plans offer a mix of stock funds, bond funds, and a money market or stable value fund. They generally do not offer exposure to real estate, commodities, or inflation protected bonds. Historically, the traditional menu of asset classes has done well and alternate options weren’t necessary. Now, we are seeing more and more 401(k) plan participants moving their assets out of their 401(k) to an IRA where they often have unlimited investment options. It is important to evaluate costs when doing so, but this may be your best bet in developing broad diversification across many asset classes. Please feel free to contact us if you’d like to review your 401(k) and overall plan for retirement.