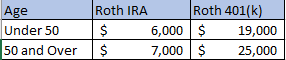

Over the past few years, Roth IRA contributions have become very popular. When you contribute to a Roth IRA you are paying federal tax now and then as long as you follow the rules for distributing the assets correctly, you never pay tax again, even on the growth. The strategy has become even more popular with recent tax reform and lower tax rates. Savers are now paying less tax up-front for tax-free growth. The problem many savers face is that you are limited in how much you can contribute to a Roth IRA or a Roth 401(k).

As you can see, the Roth 401(k) provides a huge benefit to people who want to save more on a Roth basis. The Roth 401(k) is a relatively new concept and not all 401(k) plans allow it. Not to worry though, as a participant in the above-mentioned plans you have the ability to contribute to an “After-Tax” bucket if Roth isn’t available.

The IRS also has a limit on the amount of total contributions that can be made into a retirement plan from all sources (Pre-Tax, Roth, Company Match, Profit Sharing). In 2019, if you are under 50 that amount is $56,000 and if you are over 50 it is $62,000. So to illustrate what this means, consider the below example.

Joe is over 50 and works at XYZ Company earning $175,000/year. His company offers a retirement plan with a 3% match. Joe wants to save aggressively for retirement. If he maxes out his Roth 401(k) and receives the company match, this is what his situation will look like.

Joe believes he is “maxed out” at this point because he contributed up to the IRS max on HIS contribution to the Roth 401(k). But, he still has the after-tax bucket he can use. He can save an extra $32,500 into the after-tax bucket of the retirement plan to reach the $62,000 IRS max.

Now, for the cool part. Each year, Joe can distribute the after-tax portion of the retirement plan into his own Roth IRA. This means eliminating any tax on the future growth of the after-tax money. Without moving the after-tax money to Roth, the growth would be subject to federal income tax. This essentially allows him to save $57,500 each year into a Roth IRA! That $57,500 can now grow tax-deferred and tax-free at distribution.

To learn more about this strategy, give our office a call!